-

Market Overview

2010 2nd Quarter Overview

Economy Edges Towards a Double Dip Recession

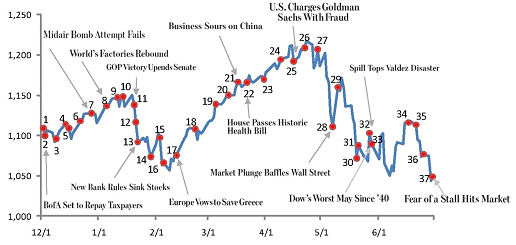

World wide economic activity slowed in the second quarter dampened by the debt crisis in Europe. The looming slowdown in the economy surprised investors and caused stock markets to decline sharply. The S&P 500 fell 12% in the second quarter. The quarterly decline broke a string of four consecutive quarterly gains. This recent dip rolled back nine months of repair that the markets logged since the end of last September. The progress of stock market recovery seems to take the stairs up but takes the elevator down.

The quarter was tumultuous. From its high level in April, the S&P is down about 16% in the span of only 8 weeks. This descent was alarming in its swiftness and magnitude.

The negative events in the quarter include the Euro debt crisis, the Goldman Sachs Fraud charge, the BP Oil Disaster, the Flash Crash, and this new and foreboding slowdown in the US economy as it threatens to lapse back into a recession. Below is a timeline:1

Government programs assisting first time homebuyers came to an end in the quarter. Federal government lifelines to various state and local governments also came to an end. Labor markets also showed signs of reversing a positive trend that has been in force since last year.

In the worldwide G-20 meeting held at the end of June, the US and other member nations all made pledges to reduce their wanton deficit spending over the next three years. This coordinated government policy, if applied, is likely to come with the unintended consequence of further weakening our economy. The complacency of policy makers coming out of that meeting shook the near term outlook for economies worldwide.

Don’t confuse the economy with the stock market

"The economy is getting stronger by the day. The economy is getting stronger by the day. The economy…". These words echoed from President Obama on June 4th.2Plenty of data would confirm this statement yet according to a Harris Poll, only 30% of US adults believe the economy will strengthen in the year ahead.

Even given the headwinds for business, a double dip recession is still unlikely. Economists and government officials including Federal Reserve members point to GDP estimates of 2.0% growth in the second quarter down from 2.7% growth in the first quarter. No one is satisfied with this slow growth but no responsible government official ever believed in a quick fix to the economic damage of the past two years. Economic recovery is destined to be slow and the unemployment rate will recover only marginally.

Contrary to conventional wisdom, the sketchy economic condition should have a very limited grip on the stock market. This poses the threat of being really good news. Over the past 18 months a growing pool of cash has accumulated outside of the stock market. This cash earns next to a zero return. Meanwhile, activity in the stock market is chiefly confined to high frequency traders, hedge funds and enterprises designed to profit from short term market moves. Once the pace of the recent decline abates, this unemployed cash will push into the stock market seeking a higher return. Cash has to be invested at some point.

All of this can happen in the context of a very weak and slow-growing economy. Similarly, it would be possible for the market to make a robust advance this current quarter without any accompanying strength in the economy. It would be the sort of syndrome where investors view the "porridge to be just right". This implies that the economy is growing slowly enough so as not to provide upward pressure on interest rates. Please look for this view to gain traction in the summer months.

One bad quarter does not make a year

At the beginning of last quarter, I provided a sanguine outlook for the stock market. I also suggested that any market weakness would be contained to around 6% based on the market’s solid historical valuation. This forecast missed its mark. Looking back, the negative events of the spring quarter generated enough fear amongst investors to cause deep and widespread selling.

It is crucial to bear in mind that we live in a rapidly changing world and sentiment as well as markets usually change course abruptly. Evidence of these shifts is found in the oil price rise in 2008, the dollar’s deterioration in 2009, and the rise in interest rates earlier this year. Those trends all reversed rapidly. Trends have a way of shifting course just when a majority of people become committed to them. Positioning for the "next" trend will prove a more fruitful way to position assets than using the most recent past as our guide.

Consistent with a rapidly changing world is one in which the stock market is most likely to have surges as well as pullbacks. Last quarter, stocks got battered much more than expected. This alone suggests the third quarter will have a different outcome. This quarter, the S&P 500 would make an 8% gain just by climbing back to where it started this year. I believe this will happen this quarter.

Peregrine Returns and Strategy

Certainly, timing major stock market moves poses a serious challenge for investment managers. Volatility can make market timing seem like a tall order. Missing a major move in the markets does not mean that the next one cannot be caught. Catching these market moves remains our aim compared to many of our competitors that concede that markets cannot be timed.

The prevailing condition of slow economic growth, low interest rates, and low nominal returns is often termed the "new normal". The byproduct of this condition is that it also implies a certain "safety net". Stocks can only retreat so far before their valuations and other conditions won’t let them fall further. These support levels provide the best interval to buy stocks. We are probably close to this level right now. Our local paper ran a doomsday forecast this week from long time bear and most fallible forecaster, Robert Prechter. Most often, bold predictions published in the media make excellent contrary indicators.

Our clients continue to be heavily weighted in equities and this drove down our client portfolios in the second quarter. A distinctively positive feature to our portfolios was our holding of long term treasury bonds which surged 14% for the quarter. These and other income oriented investments helped cushion our client portfolios from the market decline.

Last year, our client returns lagged the stock market. Over a longer haul, our Composite returns are better than the S&P 500 and the Average stock market mutual fund. The market decline in the second quarter has a good chance of setting the table for our client portfolios to start to outperform the averages and our competitors for 2010. Please stay tuned for this.

In the second quarter, our Equity Composite lost 6.38% and is now down 4.37% for 2010. This compares favorably to the S&P 500 which is down 7.14% for 2010. Our Balanced Composite fell .57% for the quarter and is still up 1.23% for 2010.

Dan Botti

Portfolio Manager

7/15/10

1 Bespoke Investment Group, LLC. "B.I.G. Tips June Headlines" 6-30-2010

2 Market Watch, "Economy the Musical" by Al Lewis 7-1-2010

Past performance is no guarantee of future results. Investment management involves the possibility of losses. Significant general stock market moves up and down can influence the performance of client portfolios. Composite returns are based on client portfolios of over $100,000. Not all clients are included in the composites. All returns include the reinvestment of dividends. All returns are net of fees. Composite returns are derived from aggregated, time-weighted returns for clients of Peregrine Asset Advisers. Individual client returns can deviate from the composite returns. While Peregrine uses the S&P 500 as a benchmark, Peregrine does not attempt to mimic the structure of this index. Individual client portfolios vary. The number of securities held also varies per client.

Do you have questions or would you like to know more, contact Dan Botti.

Overview Archive

- » 2025 2nd Quarter

- » 2025 1st Quarter

- » 2024 4th Quarter

- » 2024 3rd Quarter

- » 2024 2nd Quarter

- » 2024 1st Quarter

- » 2023 4th Quarter

- » 2023 3rd Quarter

- » 2023 2nd Quarter

- » 2023 1st Quarter

- » 2022 4th Quarter

- » 2022 3rd Quarter

- » 2022 2nd Quarter

- » 2022 1st Quarter

- » 2021 4th Quarter

- » 2021 3rd Quarter

- » 2021 2nd Quarter

- » 2021 1st Quarter

- » 2020 4th Quarter

- » 2020 3rd Quarter

- » 2020 2nd Quarter

- » 2020 1st Quarter

- » 2019 4th Quarter

- » 2019 3rd Quarter

- » 2019 2nd Quarter

- » 2019 1st Quarter

- » 2018 4th Quarter

- » 2018 3rd Quarter

- » 2018 2nd Quarter

- » 2018 1st Quarter

- » 2017 4th Quarter

- » 2017 3rd Quarter

- » 2017 2nd Quarter

- » 2017 1st Quarter

- » 2016 4th Quarter

- » 2016 3rd Quarter

- » 2016 2nd Quarter

- » 2016 1st Quarter

- » 2015 4th Quarter

- » 2015 3rd Quarter

- » 2015 2nd Quarter

- » 2015 1st Quarter

- » 2014 4th Quarter

- » 2014 3rd Quarter

- » 2014 2nd Quarter

- » 2014 1st Quarter

- » 2013 4th Quarter

- » 2013 3rd Quarter

- » 2013 2nd Quarter

- » 2013 1st Quarter

- » 2012 4th Quarter

- » 2012 3rd Quarter

- » 2012 2nd Quarter

- » 2012 1st Quarter

- » 2011 4th Quarter

- » 2011 3rd Quarter

- » 2011 2nd Quarter

- » 2011 1st Quarter

- » 2010 4th Quarter

- » 2010 3rd Quarter

- » 2010 2nd Quarter

- » 2010 1st Quarter

- » 2009 4th Quarter

- » 2009 3rd Quarter

- » 2009 2nd Quarter

- » 2009 1st Quarter

- » 2008 4th Quarter

- » 2008 3rd Quarter

- » 2008 2nd Quarter

- » 2008 1st Quarter

- » 2007 4th Quarter

- » 2007 3rd Quarter

- » 2007 2nd Quarter

- » 2007 1st Quarter

- » 2006 4th Quarter

- » 2006 2nd Quarter

- » 2005 Overview